SQ11. How has AI impacted socioeconomic relationships?

For millennia, waves of technological change have been perceived as a double-edged sword for the economy and labor market, increasing output and wealth but potentially reducing pay and job opportunities for typical workers. The Roman emperor Vespasian refused to adopt a productivity-enhancing construction technology due to its potential labor market impact;1 the Luddites destroyed textile machinery in early 1800s England;2 and, in the 1960s, arguably a golden age for the US labor market, experts warned that labor-saving technology could devastate US employment.3

And so it has been with the latest wave of innovation in the field of artificial intelligence. Though characterized by some as a key to increasing material prosperity for human society, AI’s potential to replicate human labor at a lower cost has also raised concerns about its impact on the welfare of workers. Are these concerns warranted? The answer is surprisingly murky—complex, yes, but also difficult to characterize precisely. AI has not been responsible for large aggregate economic effects. But that may be because its impact is still relatively localized to narrow parts of the economy.

The Story So Far

The recovery from the 2008–2009 recession was sluggish both in North America and Western Europe.4 Unemployment, which had spiked to multi-decade highs, came down only slowly. This weak recovery was happening at the same time as major innovations in the field of AI and a new wave of startup activity in high tech. To pick one example, it seemed like self-driving cars were just around the corner and would unleash a mass displacement of folks who drive vehicles for a living. So AI (sometimes confusingly referred to as “robots”) became a scapegoat for weak labor markets.5

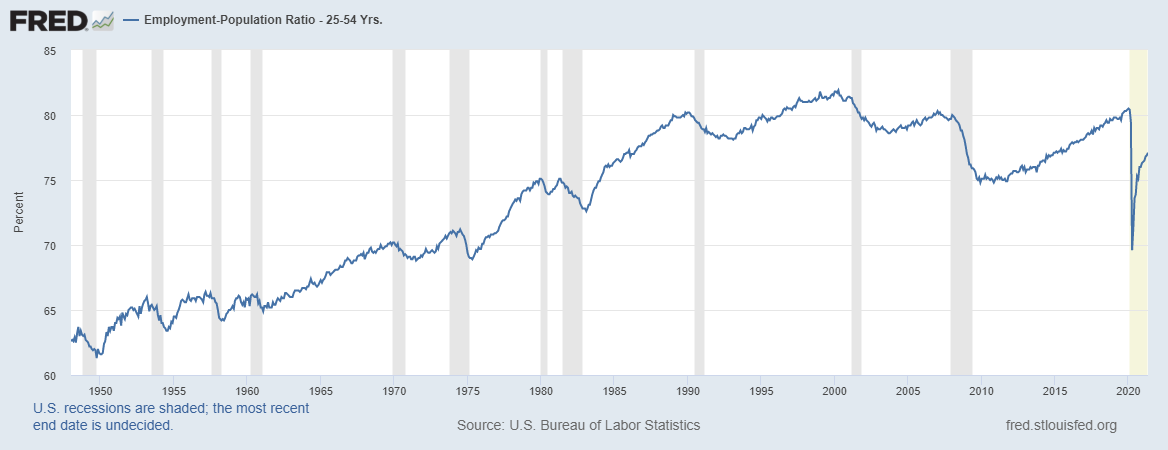

To some extent, this narrative of “new technology is taking away jobs” has recent precedents—the two prior labor market recoveries, beginning in 1991 and 2001, also started out weak, and that weakness was subsequently associated with technological innovation.6 But the possibility of applying the same narrative to the 2008–2009 recession was quickly dispelled by the post-2009 data. Productivity—the amount of economic output that can be produced by a given amount of economic inputs—grew at an exceptionally slow rate during the 2010s, both in the US and in many other countries,7 suggesting job growth was weak because economic growth was weak, not because technology was eliminating jobs. Employment grew slowly, but so did GDP in western countries.8 And, after a decade of sluggish recovery, in early 2020 (on the eve of the COVID-19 pandemic), the share of prime-working-age Americans with a job reached its highest level since 2001.9 In Western Europe, that share hit its highest level since at least 2005. The layperson narrative of the interplay between artificial intelligence technology and the aggregate economy had run ahead, and to some extent become disconnected, from the reality that economists were measuring “on the ground”.

In other words, worries by citizens, journalists and policymakers about widespread disruption of the global labor market by AI have been premature. Other forces have been much more disruptive to workers’ livelihoods. And, at least in the 2010s, the labor market has been far more capable of healing than many commentators expected.

AI and Inequality

AI has frequently been blamed for both rising inequality or stagnant wage growth, both in the United States and beyond. Given the history of skill-biased technological change may have played a role in generating inequality,10 this worry is reasonable to consider. Looking back, the evidence here is mixed, but it’s mostly clear that, in the grand scheme of rising inequality, AI has thus far played a very small role.

The first reason, most importantly, is that the bulk of the increase in economic inequality across many countries predates significant commercial use of AI. Arguably, it began in the 1980s.11 The causes for its increase over that period are hard to disentangle and are much debated—globalization, macroeconomic austerity, deregulation, technological innovation, and even changing social norms could all have played a role. Unless we are willing to call all of these disparate societal trends “AI,” there’s no way to pin current economic inequality on AI.

The second reason is that, even in the most recent decade, the most significant factors negatively impacting the labor market have not been AI related. Aggregate demand was weak in the US and many western countries during the early years of the decade, keeping wage growth weak (particularly for less educated workers). And, to some degree, impacts that are directly attributable to technology are not necessarily attributable to AI specifically; for example, consider the relatively large impact of technologies like camera phones, which wiped out the large photography firm Kodak.12

Localized Impact

In sectors where AI is more prevalent—software and financial services, for example—its labor-market impact is likely to be more meaningful. Yet even in those industries and US states where AI job postings (an imperfect proxy) are more prevalent, they only account for a one to three percent share of total postings. Global corporate investment in AI was $68 billion in 2020, which is a non-trivial sum but small in relative terms: gross private investment over all categories in the US alone was almost $4 trillion in 2020.13 It’s not always easy to differentiate AI’s impact from other, older forms of technological automation, but it likely reduces the amount of human labor going into repetitive tasks.14

How the Pie Is Sliced

Economists have historically viewed technology as increasing total economic value (making the pie bigger), while acknowledging that such growth can create winners and losers (some people may end up with smaller slices than when the entire pie was smaller). But it’s also conceivable that some new technologies, including AI, might end up simply reslicing a pie of unchanged size. Stated differently, these technologies might be adopted by firms simply to redistribute surplus/gains to their owners.15 That situation would parallel developments over recent decades like tax cuts and deregulation, which have had a small positive effect on economic growth at best16 but have asymmetrically benefited the higher end of the income and wealth distributions. In such a case, AI could have a big impact on the labor market and economy without registering any impact on productivity growth. No evidence of such a trend is yet apparent, but it may become so in the future and is worth watching closely.

Market Power

AI’s reliance on big data has led to concerns that monopolistic access to data disproportionately increases market power. If that’s correct, then, over time, firms that acquire particularly large amounts of data will capture monopoly profits at the expense of consumers, workers, and other firms.17 This explanation is often offered for the dominance of big tech by a small number of very large, very profitable firms. (And it might present an even bigger risk if “data monopolies” are allowed by regulators to reduce competition across a wider range of industries.) Yet over the past few decades, consolidation and market power have increased across a range of industries as diverse as airlines and cable providers—so, at the present moment, access to and ownership of data are at most just one factor driving growing concentration of wealth and power.18 Still, as data and AI propagate across more of the economy, data as a driver of economic concentration could become more significant.

The Future

To date, the economic significance of AI has been comparatively small—particularly relative to expectations, among both optimists and pessimists, of massive transformation of the economy. Other forces—globalization, the business cycle, and a pandemic—have had a much, much bigger and more intense impact in recent decades.

But the situation may very well change in the future, as the new technology permeates more and more of the economy and expands in flexibility and power. Economists have offered several explanations for this lag; other technologies that ultimately had a massive impact experienced a J-curve, where initial investment took decades to bear fruit.20 What should we expect in the context of AI?

First, there is a possibility that the pandemic will accelerate AI adoption; according to the World Economic Forum, business executives are currently expressing an intent to increase automation.21 Yet parallel worries during the prior economic expansion failed to materialize,22 and hard evidence of accelerating automation on an aggregate scale is hard to find.23

Second, AI will contend with another extremely powerful force: demographics. Populations are aging across the world. In some western countries, workforces are already shrinking. It may be that instead of “killing jobs,” AI will help alleviate the crunch of retiring workforces.24

Third, technological change takes place over a long time, oftentimes longer than expected.25 It took decades for electricity26 and the first wave of information technology27 to have a noticeable impact on economic data; any future wave of technological innovation is also unlikely to hit all corners of the economy at once. (This insight also helps to contextualize relative disappointment in areas like self-driving vehicles.28 Change can be slow, even when it’s real.) A “hot” labor market in which some sectors of the economy expand labor demand even as others shrink is a useful insurance policy against persistent technology-driven unemployment.

Fourth, AI and other cutting-edge technologies may end up driving inequality. We may eventually see technologically-driven mass unemployment. Even if jobs remain plentiful, the automation-resistant jobs might end up being primarily relatively low-paying service-sector jobs. In the middle of the 20th century, western governments encountered and mitigated such challenges via effective social policy and regulation; since the 1970s, they have been more reluctant to do so. To borrow a phrase from John Maynard Keynes, if AI really does end up increasing “economic possibilities for our grandchildren,”29 society and government will have it within their means to ensure those possibilities are shared equitably. For example, unconditional transfers such as universal basic income—which can be costly in a world dependent on human labor but could be quite affordable in a world of technology-fueled prosperity and are less of a disorganized patchwork than our current safety net—could play a significant role.30 But if policymakers under react, as they have to other economic and labor pressures buffeting workers over the past few decades, innovations may simply result in a pie that is sliced ever more unequally.

[1] https://penelope.uchicago.edu/Thayer/e/roman/texts/suetonius/12caesars/vespasian*.html

[2] https://en.wikipedia.org/wiki/Luddite

[3] https://conversableeconomist.blogspot.com/2014/12/automation-and-job-loss-fears-of-1964.html

[4] https://slate.com/business/2019/12/the-four-mistakes-that-turned-the-2010s-into-an-economic-tragedy.html

[5] https://money.cnn.com/2010/06/10/news/economy/unemployment_layoffs_structural.fortune/index.htm

[6] Dale W. Jorgenson, Mun S. Ho, and Kevin J. Stiroh, "A retrospective look at the U.S. productivity growth resurgence," Journal of Economic Perspectives, Volume 22, Number 1, Winter 2008 https://scholar.harvard.edu/files/jorgenson/files/retrosprctivelookusprodgrowthresurg_journaleconperspectives.pdf

[7] Karim Foda, "The productivity slump: a summary of the evidence," August 2016 https://www.brookings.edu/research/the-productivity-slump-a-summary-of-the-evidence/

[8] Edward P. Lazear and James R. Spletzer, "The United States Labor Market: Status Quo or A New Normal?" https://www.kansascityfed.org/documents/6938/Lazear_Spletzer_JH2012.pdf

[9] U.S. Bureau of Labor Statistics, Employment-Population Ratio - 25-54 Yrs., retrieved from Federal Reserve Bank of St. Louis August 26, 2021 https://fred.stlouisfed.org/series/LNS12300060

[10] This thesis is controversial: See David Card and John E. DiNardo, "Skill Biased Technological Change and Rising Wage Inequality: Some Problems and Puzzles," Journal of Labor Economics, Volume 20, October 2002 https://www.nber.org/papers/w8769; Daron Acemoglu, "Technical Change, Inequality, and the Labor Market," Journal of Economic Literature, Volume 40, Number 1, March 2002. https://www.aeaweb.org/articles?id=10.1257/0022051026976 .

[11] https://www.cbpp.org/research/poverty-and-inequality/a-guide-to-statistics-on-historical-trends-in-income-inequality

[12] https://techcrunch.com/2012/01/21/what-happened-to-kodaks-moment/

[13] Daniel Zhang, Saurabh Mishra, Erik Brynjolfsson, John Etchemendy, Deep Ganguli, Barbara Grosz, Terah Lyons, James Manyika, Juan Carlos Niebles, Michael Sellitto, Yoav Shoham, Jack Clark, and Raymond Perrault, “The AI Index 2021 Annual Report,” AI Index Steering Committee, Human-Centered AI Institute, Stanford University, Stanford, CA, March 2021 https://aiindex.stanford.edu/wp-content/uploads/2021/03/2021-AI-Index-Report_Master.pdf

[14] https://hbr.org/2016/12/wall-street-jobs-wont-be-spared-from-automation

[15] https://www.theguardian.com/technology/2019/apr/07/uk-businesses-using-artifical-intelligence-to-monitor-staff-activity

[16] https://www.everycrsreport.com/reports/R45736.html, https://www.nber.org/system/files/working_papers/w28411/w28411.pdf

[17] https://www.economist.com/leaders/2017/05/06/the-worlds-most-valuable-resource-is-no-longer-oil-but-data

[18] https://www.imf.org/-/media/Files/Publications/WEO/2019/April/English/ch2.ashx

[19] https://www.nber.org/system/files/working_papers/w24001/w24001.pdf

[20] https://www.nber.org/system/files/working_papers/w25148/w25148.pdf

[21] https://www.weforum.org/press/2020/10/recession-and-automation-changes-our-future-of-work-but-there-are-jobs-coming-report-says-52c5162fce/, https://www.theguardian.com/technology/2020/nov/27/robots-replacing-jobs-automation-unemployment-us

[22] http://www3.weforum.org/docs/WEF_Future_of_Jobs.pdf

[23] https://www.economist.com/special-report/2021/04/08/robots-threaten-jobs-less-than-fearmongers-claim

[24] https://www.nber.org/digest/jul18/automation-can-be-response-aging-workforce

[25] https://www.scientificamerican.com/article/despite-what-you-might-think-major-technological-changes-are-coming-more-slowly-than-they-once-did/

[26] https://www.bbc.com/news/business-40673694

[27] Daniel E. Sichel and Stephen D. Oliner, "Information Technology and Productivity: Where are We Now and Where are We Going?" SSRN, May 2002 https://papers.ssrn.com/sol3/papers.cfm?abstract_id=318692

[28] https://www.wired.com/story/future-of-transportation-self-driving-cars-reality-check/

[29] John Maynard Keynes, “Economic Possibilities for our Grandchildren (1930),” in Essays in Persuasion, Harcourt Brace, 1932, retrieved from https://www.aspeninstitute.org/wp-content/uploads/files/content/upload/Intro_and_Section_I.pdf

[30] Annie Lowrey, Give People Money: How A Universal Basic Income Would End Poverty, Revolutionize Work, And Remake The World, Crown Publishing, 2019 https://www.penguinrandomhouse.com/books/551618/give-people-money-by-annie-lowrey/

Cite This Report

Michael L. Littman, Ifeoma Ajunwa, Guy Berger, Craig Boutilier, Morgan Currie, Finale Doshi-Velez, Gillian Hadfield, Michael C. Horowitz, Charles Isbell, Hiroaki Kitano, Karen Levy, Terah Lyons, Melanie Mitchell, Julie Shah, Steven Sloman, Shannon Vallor, and Toby Walsh. "Gathering Strength, Gathering Storms: The One Hundred Year Study on Artificial Intelligence (AI100) 2021 Study Panel Report." Stanford University, Stanford, CA, September 2021. Doc: http://ai100.stanford.edu/2021-report. Accessed: September 16, 2021.

Report Authors

AI100 Standing Committee and Study Panel

Copyright

© 2021 by Stanford University. Gathering Strength, Gathering Storms: The One Hundred Year Study on Artificial Intelligence (AI100) 2021 Study Panel Report is made available under a Creative Commons Attribution-NoDerivatives 4.0 License (International): https://creativecommons.org/licenses/by-nd/4.0/.